The payments space continued to attract fintech investment globally; total fintech investment in APAC soared to US$7.5bn

In the first half of 2021, under pressure to increase the velocity of their digital transformation and to enhance their digital capabilities, corporations around the world have been particularly active in venture deals (close to US$21bn worth of investment over nearly 600 deals globally) believing that it is quicker to achieve transformation outcomes by partnering with, investing in, or acquiring fintechs.

According to KPMG’s fintech report for the first half (H1) of 2021, the Asia Pacific region (APAC) showed a rise in mergers and acquisitions (M&A), venture capital (VC) and private equity (PE), on top of deals activity in the first half of the year. Investments, after dropping to US$4.7bn across 357 deals in 2H 2020, have crept back up, to hit US$7.5bn across 467 deals in 1H 2021, largely driven by venture capital activity.

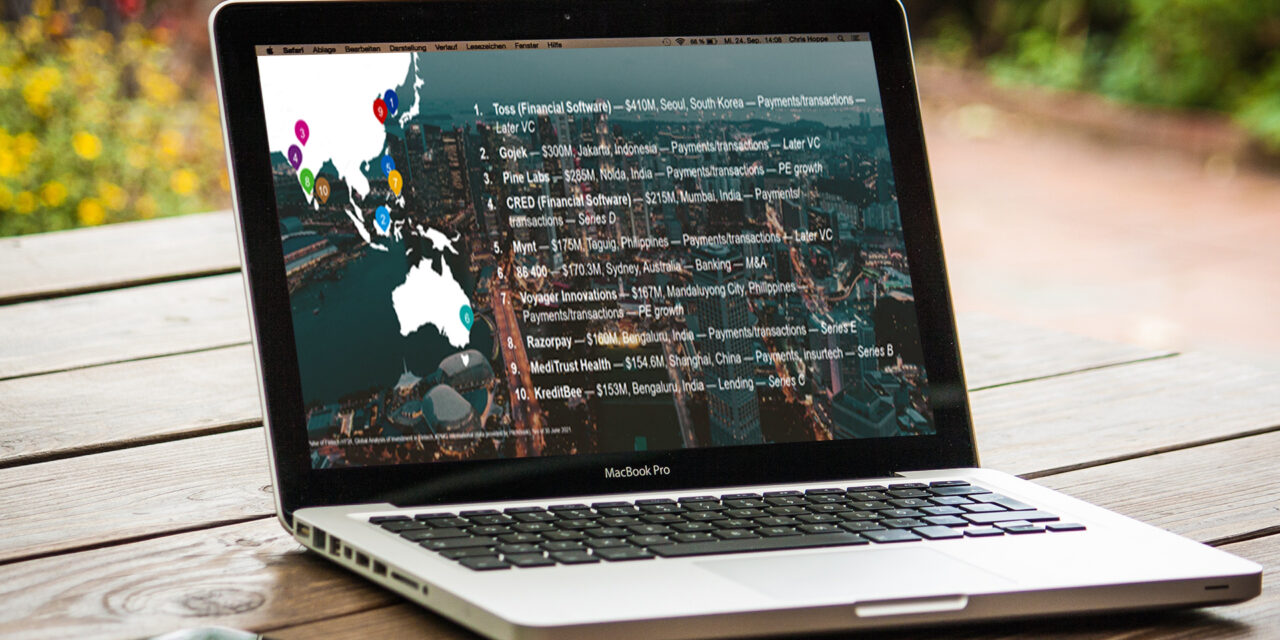

India led the way with US$2bn in total fintech investment, followed by China at US$1.3bn, Australia at US$900m, and Singapore at US$614m.

Other regional findings

- Globally, fintech investments in the payments space retained the top spot for investors’ wallets globally at US$19bn for H1 2021, compared to US$27.8bn for the entire year of 2020. Deal values for payments globally exceeded that of other fintech segments in H1 2021 such as blockchain and cryptocurrency (US$8.7bn), insurtech (US$7.1bn), regtech (US$6.6bn), cybersecurity (US$3.7bn) and wealthtech (US$1.4billion).

- Cryptocurrency and blockchain fintechs in H1 2021 transacted US$8.7bn—more than double the entire 2020’s investment figure of US$4.3bn. A significant amount of institutional money has flowed into the crypto space, highlighting the broadening of the investor base. Investor awareness and knowledge of the sector is growing in crypto assets, as well as the operational and procedural side of crypto—from custody and storage to storekeeping and the competitiveness and maturity of service providers.

- Cryptocurrency and blockchain venture capital investments have also been very strong. Numerous companies raised US$100m+ funding rounds, including BlockFi (US$350m), Paxos (US$300m), Blockchain.com (US$300m) and Bitso (US$250m).

- Globally in H1, growth in the cybersecurity space was driven bythe rise of ransomware and other cybercrime drive significant investment in the AI space, pushing cybersecurity companies to refocus their efforts on automation for cybersecurity, as well as managing and responding to incidents. Global investments into cybersecurity fintechs grew dramatically, coming in at US$3.7bn of investments in H1 2021, compared to 2020’s US$2.2bn.

- Three other areas of fintech also grew globally, as follows:

- Insurtech: This sector attracted global investments of US$7.1bn in H1 2021 compared to US$16.5bn for the entire 2020, with a lion’s share coming from the USA. Corporates have been making outright acquisitions to gain capabilities, while big techs such as Google have focused on forging partnerships to embed insurtech offerings into their platforms and products.

- Regtech: With more investors focusing on cryptocurrency trading, there was greater demand for safe and secure access to investments. The growth of digital customers and transactions during the pandemic has also driven a major increase in demand for regtech solutions that can identify and address incidents such as fraud accurately. As such, global regtech investments for H1 2021 hit US$6.6bn, as compared to US$10.4bn for the entire 2020.

- Wealthtech grew globally in H1 2021, coming in at US$1.4bn, surpassing 2020’s US$0.8bn. Corporates have continued to play a key role in wealthtech investment, with a number of well-established players making investments into or acquiring wealthtechs in recent quarters. Investing services have matured significantly and gained more credibility in the market. This is with the exception of robo-advisory which is still in its infancy: few investors have put faith in robot-driven advice over human experience.

- Among the H1 fintech investments into the payments space in APAC, ‘buy now pay later’ was one of the fastest growing sub-sectors. The strong interest of investors in the payments space has been attributed in part to an increasingly diversified payments space, which is now going beyond person-to-person and bill payments. Embedded finance solutions have become increasingly popular with payments embedded into offerings, retail apps and ecosystem platforms. Also emerging in the payments space are disbursements which are being looked at both by insurers for claims processing and by governments as part of disaster recovery.

- In Singapore’s fintech industry, a total of 72 deals worth US$614.2m were transacted from January to June, a 22% per cent increase from 59 deals in 1H 2020, compared to the 48 deals in 1H 2019. Deal numbers for the H1 2021 are the highest since 1H 2018. Dry powder cash reserves, increasing diversification in hubs and subsectors, and strong activity across the world contributed to the record start to 2021.

- Despite more fintechs deals occurring in Singapore fintechs, the amounts involved were smaller compared to last year, which totaled US$1.02bn. A large part of H1 2020’s total deal value were from the US$856m deal scored by Singapore-based firm Grab.

- In APAC, platform players with strong fintech offerings continued to be very strong, with many working to build their breadth, reach and market share. Aside from Grab, Indonesia-based Gojek had also raised funds (US$300million) in 1H 2021 and announced a merger with Tokopedia for US$18bn to create the GoTo Group.

- There has been a year-on-year downward trend of investment figures by corporates and their venture arms in APAC. They invested US$24.9bn in fintechs in 2018, compared to US$10.3bn in 2019 and US$7.9bn in 2020. H1 2021 saw just US$2.8bn invested.

- Over the next six months, start-ups, including mature fintechs in the Asia-Pacific region, are expected to see more interest from US-based special purpose acquisition companies. In H1, Grab announced the largest SPAC merger ever, over a US$40bn deal with US-based Altimeter Growth Corp.

In the next half of 2021, KPMG expects total fintech investment to remain very robust in most regions of the world. While the payments space is expected to remain a dominant driver of fintech investment— revenue-based financing solutions, banking-as-a-service models, and B2B services are expected to attract increasing levels of investment.

Given the rise in digital transactions, and the subsequent increase in cyberattacks and ransomware, cybersecurity solutions will likely also be high on the radar of investors.

Said Anton Ruddenklau, KPMG’s Global Fintech Co-Lead: “As we head into H2 2021, we anticipate more consolidation will occur, particularly in mature fintech areas as fintechs look to become the dominant market player either regionally or globally.”

{kind=link}