Large corporates and small fintech startups need each other despite the pressures to be faced after the pandemic, says this expert.

As the pandemic continues to create uncertainty across sectors, fintech companies are being tested for resilience, rigor of business models and operations, cost and expense management, and the ability to win and sustain investor interest for funding.

At the same time, interest rate cuts and the global economic slowdown are impacting the banking sector and radically changing many industry assumptions—for example, the need for large banks to engage with fintechs being one of them in the immediate short term while efforts are focused on containing and rationalizing the risks and costs of the current environment.

It also does not help that partnerships between fintechs and industry incumbents are often not organic or easy. Realizing a partnership’s upside takes time and scale, which contributes to the growing hesitation during this time period towards spending valuable resources to enter them.

This reticence, while understandable, will be costly in the long-run, particularly as millions of people emerge out of COVID-19 being more digital, cashless and e-commerce oriented than before.

As the broader economy shifts from respond to recover, COVID-19 will compel increased collaboration between fintechs and industry incumbents to meet the need for digital services, distribution and engagement experiences.

Collaborations will need to be different

These collaborations will need to pick up pace to align with the numerous ways that consumers and businesses have changed in the last few months. Regulators and financial services institutions —as they reimagine growth and adapt rapidly to the more highly digital ecosystem—will further drive and align with the rising trend towards open banking.

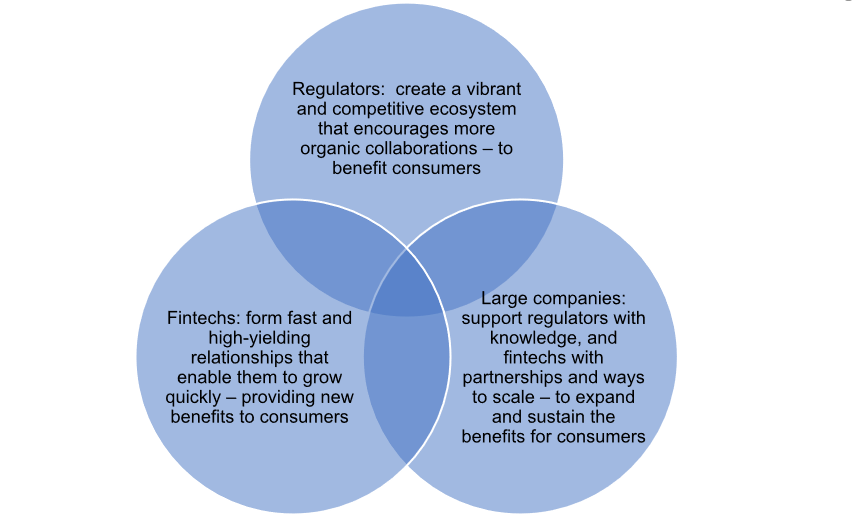

As a result, tomorrow’s partnerships need to be more organically successful. For them to be so, it is critical that all stakeholders focus on what they have in common—the aim to benefit consumers and grow their businesses.

Within these interlocking relationships, valuable opportunities for collaboration are lost when agile tech players with young founders see themselves as pitted against large institutions with set and slow practices; they could consider themselves in pursuit of opportunities for shared growth instead.

Likewise, large corporates can miss out on new projects with rich potential if they stay too focused on minimizing risk. In this current environment, regulators can support the ecosystem better by creating more systemic vehicles that better catalyze healthy partnerships.

On the other hand, when partnerships do come together— with each party believing they can make better products and services for the consumer together—and take a shared leap of faith in that direction, this shared purpose will have enormous impact on consumers’ lives and the financial services market. Purpose-driven relationships around superordinate goals have the ability to overcome many of the friction-causing challenges, from negotiating compliance standards and security risks to cultural mismatches with their partner.

Building successful partnerships

Let me give you a couple of examples. Mastercard and fintech firm Rapyd partnered last year through Mastercard’s new rapid fintech onboarding process, Fintech Express, with the purposeful aim of enabling and accelerating innovation across the region.

Rapyd brings to the table its “Fintech-as-a-Service” offering, which removes the back-end complexities of cross-border commerce and provides local payments expertise for developers, small and larger players in the gig economy.

Mastercard’s technology strengthens that offering and extends the reach of that service. In another example, fintechs providing loans to the underbanked and to SMEs can deliver the funding to the final recipient via a Mastercard to enable them to spend the loan amount digitally, as required.

To bring more of these kinds of successful partnerships together with speed, agility and effectiveness, all players in the financial services ecosystem should consider the following:

- In the short-run: Resume seeking high-impact partnerships with similarly-minded organizations for purpose-driven consumer-benefiting initiatives, particularly in the area of supporting SMEs, bolstering supply chains, and helping accelerate the financial and digital inclusion of individuals during the COVID-19 pandemic.

- In the medium-term: Learn, share, adapt and grow these partnership initiatives into relevant areas of longer-term growth. Take the lessons learned and possibilities opened, and design your solutions for shared problems with your partners from the ground up. As you reconsider your post COVID-19 business models, partner by design.

- In the long-term: Leverage these partnerships to co-connect with your customers long-term as well as keep strategic pace with the many changes that will inevitably continue happening during COVID-19 and thereafter.

While the COVID-19 environment is complex and unpredictable for many, it is also exposing vulnerabilities and raising awareness that collaboration is the only way to solve them. This presents players in the financial services industry with many opportunities to embrace the challenges to build a stronger ecosystem together.

Those who do, and develop new partnerships along the way with purpose, will not only be instrumental in helping through the crisis, but will also emerge from this time with stronger industry and commercial relationships—all to the benefit of the consumer.

{kind=link}